Stop Blind Quoting: Why Your Proposals Lose To Agents Who Actually Look

The email came in on a Monday: "I've got five vehicles and a home, what can you do for me?" Solid prospect. Multi-line bundle. The kind of opportunity that should be straightforward.

It was anything but.

Over the next week and a half, the agent went back and forth with this prospect in a slow drip of one-liner emails. First came a vague description of coverage. Then a screenshot of someone else's quote -- no context, no current policy, just a number. Three days later, a blurry photo of what might have been half a declarations page. Then silence. Then another one-liner: "So what do you think?"

Here is what every other agent working that same prospect was probably doing: grabbing the screenshot, plugging a number into their rater, and sending back a quote that was a few dollars cheaper. Blind quoting. No idea what the prospect's current deductibles looked like, whether liability limits were adequate for a high-value home, or what gaps might be hiding in a five-vehicle policy cobbled together over years of add-ons.

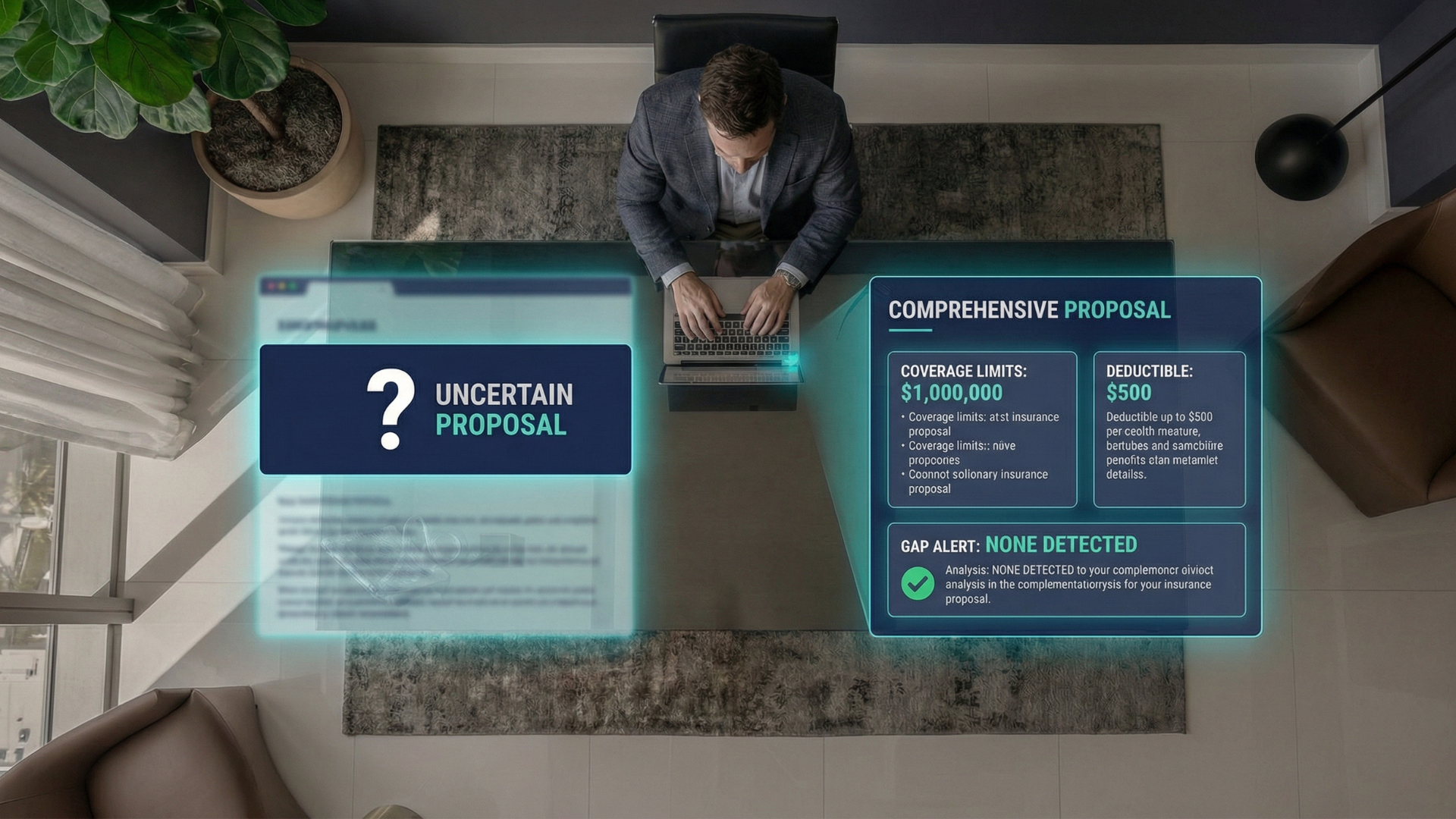

This agent did something different. After the fourth or fifth email volley, he stopped. He told the prospect, plainly: "We've gone back and forth on this for a while now. Let me actually see what you have so I can figure out what you need." He sent a single link.

The prospect clicked it that evening. By the next morning, the agent had structured policy data for every vehicle and the home -- coverage limits, deductibles, carrier details, claims history. Not screenshots. Not summaries. Complete, accurate data he could actually work with.

And what he found was telling. Coverage gaps the prospect did not know existed. A deductible structure that made no sense given the home's value. An umbrella policy that probably should have been in place and was not. None of this was visible in the screenshots. None of it would have surfaced in a blind quote.

The real cost of quoting in the dark

When you quote off incomplete information, you strip yourself of every advantage you have as an agent. You are not advising anymore. You are just pricing. And pricing is a game you will lose, because someone will always be cheaper -- or at least appear cheaper when the prospect does not understand what they are actually comparing.

The math makes the case. Insurance lead conversion rates sit between 8% and 15%, which means the vast majority of quotes go nowhere. A blind quote has even worse odds because it gives the prospect no reason to choose you over the next agent who also sent a number without context.

Nobody goes shoe shopping barefoot. You would not walk into a store and say "give me something in a size" without knowing what size. But that is exactly what blind quoting is -- guessing at coverage based on fragments, then hoping the price is right.

The agent who stopped the email chain and asked to see the full picture did not win on price. He won because he could point to specific things: "Your liability limits are too low for a property worth this much. You do not have gap coverage on the newer vehicles. Here is a claim that is going to age off your record in fourteen months, which changes your rate." The prospect's response was one the agent heard more than once: "Nobody else even mentioned those."

That is the difference between a blind quote and an informed proposal. One competes on a number. The other competes on knowledge. And with AI adoption in insurance jumping from 8% to 34% year over year, agents who still rely on screenshots and guesswork are falling further behind every quarter.

What actually seeing the policy looks like

The fix is not complicated, but it does require a different first move. Instead of asking for photos or waiting for fragments to trickle in, agents can use InsurGrid's secure data collection link to let prospects connect their insurance accounts directly. The system pulls dec pages, coverage limits, deductibles, and carrier details into a structured format -- accurate and complete, without a single phone call about "can you send me page two of your dec page?"

From there, AI-powered policy intelligence flags gaps, misaligned coverage, and cross-sell opportunities automatically. The agent is not digging through PDFs. The agent is reviewing a clear picture of what the prospect has and what they are missing.

The takeaway is simple. The next time a prospect sends you a screenshot and asks "what can you do," resist the urge to quote back immediately. Ask to see the full picture first. You will lose the prospects who only care about the lowest number -- and you were going to lose them anyway. You will win the ones who actually want an agent, not a vending machine.

.svg)